Is real estate tax the same as property tax? In most places, the two terms describe the same local tax on land and buildings, with only minor differences depending on the state. Some states also tax personal property, for example vehicles or business equipment, which is different from real estate. Read on for clear definitions, examples, and savings tactics.

Real estate tax vs property tax, the basics

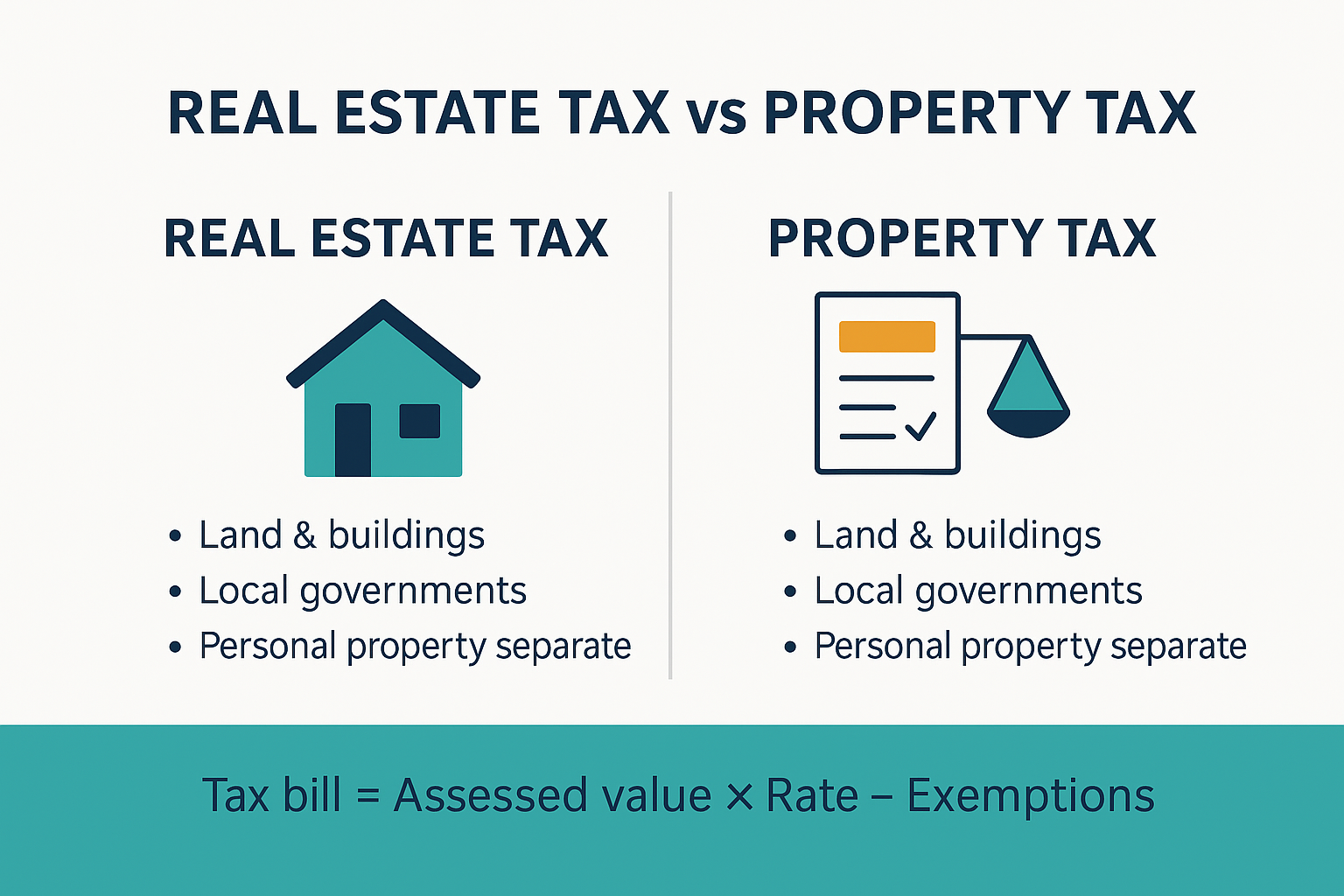

For a homeowner, these terms almost always point to the annual tax charged by your city or county on real property, meaning land plus anything attached to it, for example a house or garage. Local governments use this revenue to fund schools, roads, police and fire departments, parks, and special districts.

Why the mix up? States use different labels. Many assessors publish bills as property tax. Some handbooks call the same levy real estate tax. In everyday usage the two are interchangeable for homes and buildings. The only wrinkle is personal property tax. A few states levy a separate tax on personal property, for example cars, boats, or a business’s machinery. That is not a tax on real estate, even though it is often grouped under the wider label property tax.

If you want a deeper comparison of terminology and scope, see your internal guide on real estate tax vs personal property tax.

Key differences and similarities at a glance

| Topic | Real estate tax | Property tax |

| What is taxed | Land and improvements (homes, buildings, permanent structures) | Often the same as real estate, plus in some states personal property like vehicles or business equipment |

| Who charges it | Usually county, city, township, and special districts | Same set of local authorities |

| How value is set | Assessed value based on market data, mass appraisal methods, and state rules | Same, but may include separate schedules for personal property where applicable |

| Appeal path | Assessor review, local board, sometimes state board or court | Same process, with extra forms for personal property where it exists |

| Common exemptions | Homestead, senior, disability, veteran, agricultural, religious or charitable uses | Same exemptions for real estate, personal property exemptions vary by state |

Note: If your state taxes personal property, your bill or portal usually separates real estate from personal property. The assessment notices, due dates, and penalties may differ.

How the tax is calculated?

All jurisdictions follow a simple structure.

Tax bill = Assessed value × Assessment ratio (if any) × Mill rate or tax rate, after exemptions and credits

- Assessed value: The assessor’s estimate of your property’s market value for tax purposes.

- Assessment ratio: Some states tax a fraction of market value, for example 80 percent.

- Mill rate or tax rate: Published as dollars per 1,000 of assessed value, or as a percentage.

- Exemptions and credits: Reductions for homestead, senior status, veterans, and others.

Example calculation you can adapt

- Market value: 400,000

- Assessment ratio: 80 percent

- Assessed value: 320,000

- Combined local rate: 1.25 percent

- Homestead exemption: 25,000

Taxable value equals 320,000 minus 25,000 equals 295,000.

Estimated bill equals 295,000 times 0.0125 equals 3,687.50.

Tip: For quick comparisons across neighborhoods, use the effective tax rate. Divide last year’s bill by last year’s market value. That gives you a percent that is easy to scan on listings.

Exemptions, credits, and relief programs

Most homeowners do not pay the full headline rate, because exemptions reduce the taxable value.

- Homestead exemption: For primary residences. Reduces assessed value or applies a credit.

- Senior or disability exemptions: Extra reductions for eligible groups, sometimes with income limits.

- Veteran exemptions: Often generous for service connected disability.

- Agricultural or open space: Preferential assessment based on land use rather than market value.

- Circuit breaker credits: When taxes exceed a set share of income, you may receive a state income tax credit or a direct refund.

Action: Search your county assessor’s site for “exemptions”, then calendar the renewal date so you never lose benefits. If you manage multiple properties, add a checklist in your internal playbook for property tax management.

Assessment, reassessment, and how to challenge an error

How assessors estimate value

Assessors rely on mass appraisal. They group similar properties and use sales data, cost models, and income approaches for rentals. They adjust for square footage, location, age, renovations, and condition.

Signs your assessment might be off

- The assessor lists more bedrooms or a larger lot than you actually have.

- Your home is valued above recent sale prices of close comparables.

- A major defect or storm damage is not reflected in the record.

- The property is owner occupied, but the file shows “non homestead”.

Step by step appeal path

- Audit the record. Print your property card and note any factual errors.

- Collect comparables. Target recent, arm’s length sales within a similar school zone and age range.

- Run the math. Apply the same adjustments the assessor uses, for example price per square foot, or market supported adjustments for garages and basements.

- File on time. Many jurisdictions allow only 10 to 45 days after notice.

- Start at the assessor’s office. Many corrections are resolved informally if you bring clear evidence.

- Proceed to the board. If needed, present your packet to the local board, then to state boards or court.

Pro move: Include a short reconciliation table that averages three valuation approaches: sales comparison, cost less depreciation, and income (for rentals). Boards appreciate a clean, consistent story.

Savings playbook for homeowners and investors

For owner occupants

- Claim every exemption you qualify for. If you split time between two homes, you generally get one homestead only.

- Watch for “non homestead” coding after refinancing. Lenders sometimes trigger a classification change. Fix it quickly to avoid higher rates.

- Ask about installment plans. If cash flow is tight, many treasurers offer partial payment plans.

- Time renovations with reassessment cycles. Large additions can raise value. If your jurisdiction reassesses on a fixed cycle, understand the timing.

For landlords and short term rental owners

- Class matters. Rental classification can have a different rate than owner occupied. Budget accordingly.

- Document capital improvements. If your property suffers unusual functional obsolescence, detailed photos and contractor reports help your case.

- Use the income approach. Present rent rolls, vacancy assumptions, and market cap rates to support a lower value.

- Track special assessments. Streetscapes and utility projects can add separate line items. Appeal if the benefit is overstated.

Budgeting, cash flow, and escrow

- Escrow through your lender. Most mortgages include a monthly escrow for taxes and insurance. Lenders true up annually.

- Self managed payment plans. Where monthly plans are allowed, set auto pay to avoid penalties.

- Forecast increases. New school bond? Reappraisal year? Add a conservative buffer, for example 5 to 10 percent, in your annual budget.

Callout: Consistent, centralized tracking is the backbone of effective property tax management. If you manage multiple doors, keep a shared calendar with due dates, appeal windows, and exemption renewals.

Common myths to avoid

- My neighbor’s lower bill guarantees mine will match. Homes can differ in size, renovations, or exemptions.

- A recent purchase price is the only value that counts. Assessors consider market evidence across many sales, not one isolated transaction.

- Appealing will raise my taxes. Corrections for factual errors should not trigger punitive increases.

- Skipping the homestead now will let me stack it later. Most programs do not allow retroactive stacking. Claim as soon as you qualify.

Practical checklist you can copy

- Pull your latest assessment and verify facts line by line.

- Calculate your effective rate from last year’s bill.

- Compare at least three recent sales within your school zone and size range.

- File or renew exemptions before the deadline.

- Map out due dates and appeal windows for the next twelve months.

- If your state taxes personal property, confirm whether any vehicles or business assets are listed under a separate account.

For aspiring agents and real estate professionals

Understanding local tax mechanics helps you explain total cost of ownership. If you plan to go pro, read the internal guide on the cost to get real estate license in your state, then build a repeatable client script that covers taxes, insurance, utilities, and HOA dues.

Real estate tax tips you can apply this year

Here is a compact list you can bookmark. For a deeper dive see your internal resource on real estate tax tips.

- Bundle photos and receipts for any condition issues before appeal season.

- Verify your classification after refinancing or title changes.

- Apply for senior, disability, or veteran relief as soon as you qualify.

- Audit any special assessment for accurate frontage or benefit calculations.

- If reassessment just spiked values, study your jurisdiction’s phase in rules. Many areas smooth increases over multiple years.

- For rentals, track net operating income carefully. Lower NOI can support a lower value under the income approach.

FAQ

Is real estate tax the same as property tax?

Usually yes, for homes and buildings the terms are used interchangeably. The exception is personal property tax in some states, which covers things like cars or business equipment.

What is personal property tax?

A separate tax in certain states on movable property, for example vehicles or machinery. It is not a tax on land or buildings. Your bill or portal normally lists it on a different account.

How do I estimate my annual property tax quickly?

Multiply your home’s value by the effective tax rate in your area. If the rate is 1.2 percent and the home is worth 350,000, a fast estimate is 4,200. Then subtract any exemptions to adjust.

What is the difference between assessed value and market value?

Market value is what a buyer would likely pay today. Assessed value is the number the assessor uses for taxes. In some states assessed value equals a fixed percentage of market value.

When should I appeal?

Appeal when the facts are wrong, or when comparable sales show your assessment is materially higher than market value. File within the posted window on your notice.

Can I lower my bill without moving?

Yes. Claim exemptions, correct classification errors, and appeal inflated assessments. If your jurisdiction allows it, choose installment plans to smooth cash flow.