When most people think about an auto loan calculator, they only see a car buying tool. You plug in a price, a rate, a term, and check whether the monthly payment feels comfortable today.

For anyone serious about real estate, construction financing, or business growth, that is not enough.

Your car payment shows up every time a lender looks at you for:

- A residential mortgage

- Investment property financing

- Personal or business construction loans CFS

- A business construction loan for a development or commercial project CFS

Used properly, an auto loan calculator becomes a planning dashboard. It lets you design a car loan that supports your long term goals instead of quietly weakening your borrowing power.

In this guide, we will connect your auto loan decisions directly to:

- Home purchase and refinance strategy

- Equity access and renovation planning

- Construction and business lending options

Understanding The auto loan calculator In A Real Estate Context

An auto loan calculator estimates your monthly payment and total cost based on a few key inputs. When you look at those numbers through a real estate lens, they become early warning signals about your future borrowing capacity.

Core Inputs And Why They Matter For Property Buyers

| Calculator Field | What You Enter | Why It Matters For Real Estate And Construction |

|---|---|---|

| Vehicle price | Contract price of the car | Higher price means a larger loan competing with future mortgage or project debt |

| Down payment | Cash you pay upfront | Bigger down payment lowers your loan balance and monthly obligation |

| Interest rate (APR) | Annual rate on the loan | Higher rate increases monthly payment and total interest cost |

| Loan term | Length of the loan in months, for example 36, 60, 72 | Longer term reduces monthly payment, but keeps debt on your books for more years |

| Taxes and fees | Sales tax, registration, documentation fees | May be financed, increasing the loan, or paid from cash that could be saved instead |

From these inputs, the calculator gives you:

- Estimated monthly car payment

- Total cost of the loan

- Total interest paid over the term

For real estate and financial services planning, the most important outputs are:

- Monthly payment, which directly affects your debt to income ratio (DTI)

- Loan term, which tells you how long that payment will restrict your cash flow

Key idea

Treat the auto loan calculator as a debt allocation tool, not just a car payment checker. Every dollar you lock into a vehicle is a dollar you cannot allocate to a home, rental property, or development project.

How Auto Debt Affects Mortgages And Construction Financing

Whether you are applying for a traditional mortgage, seeking construction loans for a build, or structuring a business construction loan through your company, lenders always look at your existing obligations. CFS+1

Debt To Income Ratio, The Bridge Between Car And Property

Your DTI compares your monthly debt payments to your gross monthly income. It typically includes:

- Mortgage or rent

- Auto loans and leases

- Student loans

- Credit card minimums

- Personal and business loans where you are personally liable

The higher your fixed car payment, the less room remains for:

- A primary home mortgage

- Investment property loans

- Additional credit that may be needed during a build or renovation

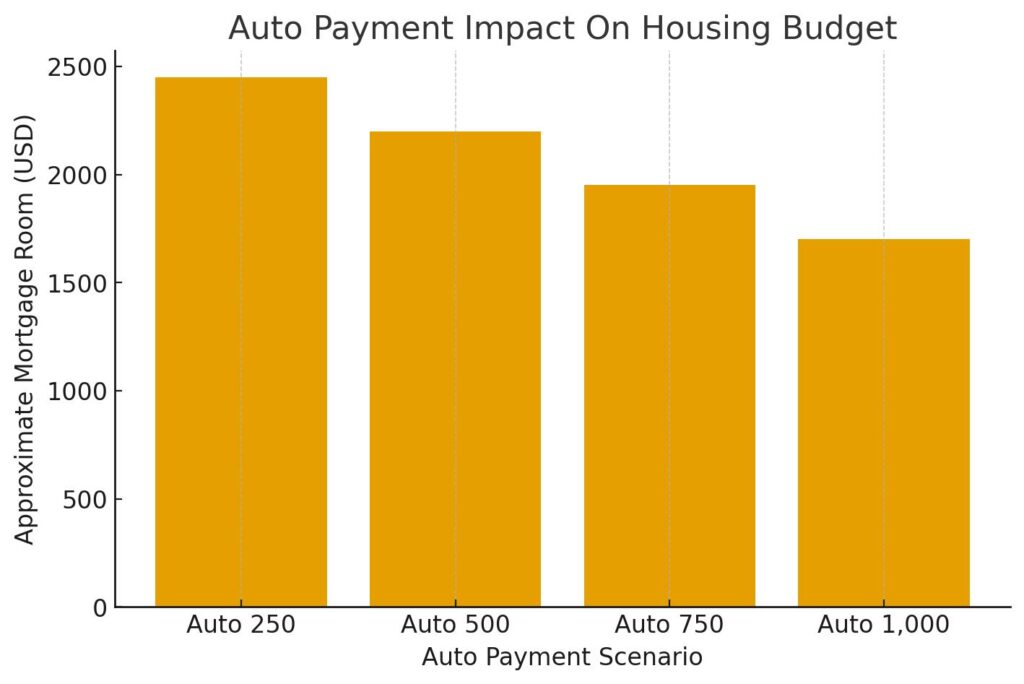

Visual Comparison, Auto Payment Impact On Housing Budget

Assume:

- Gross monthly income: 7,500 dollars

- Lender comfortable with total debt at 40 percent of income: 3,000 dollars

- Other non auto debts: 300 dollars per month

Or in table form:

| Scenario | Auto Payment | Other Debts | Total Debt Limit | Room Left For Housing Payment |

|---|---|---|---|---|

| 1, Very modest car | 250 | 300 | 3,000 | 2,450 |

| 2, Comfortable modern car | 500 | 300 | 3,000 | 2,200 |

| 3, Higher end vehicle | 750 | 300 | 3,000 | 1,950 |

| 4, Luxury focused choice | 1,000 | 300 | 3,000 | 1,700 |

The same income and same lender rules produce very different mortgage budgets, purely based on car choice. That change flows straight into:

- How much home you can buy

- How aggressively you can invest in additional units or commercial property

- How conservative you look when applying for construction or business credit

Step By Step, Using An auto loan calculator With A Real Estate Mindset

Instead of starting from the car you want, start from the property portfolio you want.

Step 1, Define Your Property And Financing Goals

Clarify the next few major moves you want to make:

- Buy your first home

- Upgrade to a larger property

- Acquire a rental unit or small multifamily

- Apply for construction loans for a development CFS

- Secure a business construction loan to build or expand a business asset CFS

For each goal, think about:

- Rough timeline, such as 2 years, 3 to 5 years

- Estimated monthly housing or project debt you are comfortable with

- Minimum savings or cash reserve you want to maintain

Step 2, Choose A Maximum Car Payment Instead Of A Car First

Work backwards from your goals to decide a safe upper limit for your car payment.

Simple approach:

- Estimate a healthy maximum for total monthly debt, for example 35 to 40 percent of gross income

- Subtract your future target housing or project payment

- Subtract existing long term debts

- The remaining number is maximum non housing debt, including your car

You then decide how much of that remaining capacity you are willing to allocate to an auto loan versus leaving unused for safety and flexibility.

Step 3, Model Car Scenarios In The auto loan calculator

Now use the calculator to test combinations until they fit within your chosen ceiling.

| Option | Price | Down Payment | Rate | Term (months) | Estimated Payment | Strategic Fit |

|---|---|---|---|---|---|---|

| New compact car | 28,000 | 4,000 | 7.5 % | 60 | About 480 | Works if you want a moderate payment |

| Certified pre owned mid size | 24,000 | 5,000 | 7.0 % | 60 | About 378 | Strong, leaves room for mortgage and savings |

| Reliable used car | 18,000 | 4,000 | 7.5 % | 48 | About 335 | Very strong, ideal if planning a major project |

Do not stop when the calculator shows a payment that simply feels affordable. Ask:

If I carry this payment for the full term, will it support or delay my next property or construction move?

Step 4, Align Loan Term With Your Real Estate Timeline

A low car payment with a very long term can still cause problems if it overlaps with key milestones:

- Mortgage application

- Pre qualification for a renovation or equity product

- Business loan underwriting for a new building or expansion

Ideally:

Or you should plan pre payments and principal reductions so that your DTI looks cleaner at application time

Your auto loan should end, or be significantly reduced, before a major property purchase or large project

Combining auto loan calculator And home equity loan calculator In One Strategy

Once you own property, another planning tool becomes important, a home equity loan calculator.

Even if your site hosts that calculator on a different page, both tools serve the same purpose, making invisible trade offs visible.

Two Calculators, One Balance Sheet

| Tool | Main Question It Answers | Typical Use Case In Your Plan |

|---|---|---|

| auto loan calculator | How much will this car cost me each month and in total | Before committing to a vehicle, to protect borrowing power |

| home equity loan calculator | How much can I borrow against my property, and at what cost | After owning property, to fund renovations or other investments |

Used together, they help you:

- Limit consumer debt that weakens your profile

- Unlock property backed capital at the right time and size

- Decide whether to direct extra cash to auto payoff, mortgage reduction, or future projects

Practical callout

When you are a few years into homeownership, compare two paths in a simple spreadsheet:

1, Paying off your auto loan faster, using the auto loan calculator to estimate savings on interest.

2, Keeping the car payment schedule, and using the home equity loan calculator to see what an equity draw could fund, such as value adding renovations.

How Auto Debt Looks To Real Estate And Construction Lenders

CFS and similar firms look at your story in numbers. Existing articles like the High Risk Business Loans Checklist and Construction Loan Guides highlight how lenders assess risk, collateral, and repayment capacity. CFS+1

Your auto loan is part of that story.

Residential Mortgage Underwriting

For a home loan, underwriters usually check:

- Stability of income

- DTI ratios with current and proposed debts

- Credit history and utilization

A large car payment:

- Reduces allowable mortgage size

- May force you into a smaller property than your income alone would support

- Can raise questions about financial priorities if combined with limited savings

Construction Loans For Personal Projects

If you are seeking construction loans to build a new primary residence, add an extension, or renovate a multi unit property, the lender wants to know that:

- You can handle unexpected cost overruns

- You will still be comfortable making interest only or blended payments during the build

- You are not already stretched by other fixed obligations

A carefully planned auto payment, visible through your auto loan calculator assumptions, supports your case.

Business Construction Loan For Developers And Owners

For a business construction loan, lenders evaluate both the project and the person behind it:

- Project feasibility and exit strategy

- Collateral and loan to value ratios

- Sponsor strength, experience, and personal financial position

If your personal balance sheet shows a very high car payment relative to income, it signals:

- Potential lifestyle creep

- Less resilience if business cash flow tightens

- Additional pressure on credit in a downturn

By running conservative scenarios in an auto loan calculator before upgrading vehicles, you protect your credibility as a borrower when larger opportunities appear.

Use Case Columns, How Different Clients Should Use The auto loan calculator

| Profile | Main Goal | How To Use The auto loan calculator Strategically |

|---|---|---|

| First time homebuyer | Qualify for a starter home sooner | Cap car payment at a low percentage of income to keep DTI flexible |

| Move up buyer with family | Upgrade to a larger home within 3 years | Choose a term and payment that will fall or end before the purchase |

| Small landlord or investor | Acquire additional rental units | Keep auto payment modest, redirect savings to down payments and reserves |

| Small construction firm owner | Qualify for business construction loan funds | Maintain a conservative car loan so business financials look stronger |

| Established business owner | Combine property expansion with equipment finance | Use both auto and equipment calculators to avoid over layering fixed debt |

Common Mistakes When Using An auto loan calculator

Many people make the same errors when they first use this tool.

1, Only Checking Whether The Payment Feels Comfortable Today

They do not test:

- How the payment affects future mortgage approval

- How it fits alongside potential project debt

- What happens if income drops or expenses rise temporarily

2, Ignoring Total Interest And Opportunity Cost

A longer term with a slightly lower monthly payment can:

- Add thousands in extra interest

- Delay the point when you can redirect that cash to investments, renovations, or land acquisition

3, Not Stress Testing For Rate And Income Changes

Smart planning means manually adjusting:

- Interest rate a little higher than the best offer

- Income a little lower than current level

- Savings target a little higher than your minimum

If the payment only works in a perfect scenario, it is not a strategic choice.

4, Overlapping Big Decisions

Another error is stacking major moves:

- New high payment car

- Plus a home purchase

- Plus a renovation or construction loan

- Plus a new line of business credit

The calculator lets you simulate all of these, but you need to apply discipline in the order and timing of commitments.

Local Angle, Boston auto loan FAQs And Market Sensitivity

If you are in a higher cost market like Boston, auto decisions are even more sensitive, because property prices and taxes eat a larger share of your budget.

A resource similar to Boston auto loan FAQs can help educate local buyers on: CFS

- Typical auto and mortgage DTI expectations in the region

- How lenders in New England view different types of consumer debt

- Practical payment ranges that leave room for Boston area housing costs

Example Questions Worth Including In A Boston Focused FAQ

- What percentage of my gross income should go to car payments if I plan to buy in the Boston metro area

- How does a paid off car affect my approval odds for a condo or multifamily in dense neighborhoods

- Should I delay a car upgrade if I am within 12 months of applying for a renovation or construction loan

You can repurpose short answers from this article into FAQ entries or snippets for that local content hub.

Summary Table

The following table summarizes the main concepts in a format that works well both for readers and for AI powered tools that might repurpose your content into snippets, checklists, or calculators.

| Entity / Concept | Type | Short Definition | Typical Use In A Plan |

|---|---|---|---|

| auto loan calculator | Tool | Estimates car payments based on price, rate, term and fees | Set a safe payment that protects DTI and cash flow |

| home equity loan calculator | Tool | Estimates borrowing power against home equity | Plan renovations, debt consolidation, or new investments |

| Debt to income ratio | Metric | Total monthly debt divided by gross monthly income | Determines mortgage and construction loan capacity |

| Construction loans | Product | Short or medium term loans to fund building or renovation | Finance development or major upgrades safely |

| Business construction loan | Product | Construction financing arranged through a business entity | Build or expand income producing assets |

| Boston auto loan FAQs | Content cluster | Local FAQ style content about auto loans and housing impact | Educate buyers in high cost markets on safe debt levels |

| Car loan term | Attribute | Number of months until the auto loan is fully repaid | Align with property purchase or refinance timeline |

| Total interest paid | Metric | Sum of all interest over the life of the loan | Compare aggressive vs conservative auto financing strategies |

You can easily convert this table into structured data, internal calculators, or lead qualifying tools.

Conclusion, Treat Your auto loan calculator As Part Of Your Real Estate Toolkit

An auto loan calculator is not just for car shoppers. For anyone working with real estate, renovation, or construction finance, it is a front line planning tool that helps you:

- Keep your debt to income ratio in a lender friendly range

- Protect your ability to qualify for mortgages, construction loans, and business construction loan products when the right opportunity appears

- Coordinate car purchases with equity planning using tools like a home equity loan calculator

- Present a disciplined, strategic financial profile rather than a reactive one

The next time you open an auto loan calculator, do not just ask, “Can I afford this car today?”

Ask, “Will this payment support or slow down my overall financial strategy and property goals?”

That one question, supported by careful use of the calculator, can make the difference between a car that simply looks good now and a financial plan that actually works over years of real estate and business growth.