When planning a build or renovation, securing favourable construction loan rates can make the difference between a smooth project and budget-blowouts. This article walks you through how rates are set, what you can control, and the strategies to lock in the best deal. Along the way we’ll touch on related concepts like a commercial construction loan, owner builder construction loans, business construction loan and how to use a home construction loan calculator.

Understanding What Construction Loan Rates Mean

What is a construction loan?

A construction loan is a short-term financing vehicle used to fund the building (or major renovation) of property before it converts into a permanent mortgage or is paid off. The lender releases funds in stages (draws) as construction progresses.

Because the project is in flux and collateral is incomplete, lenders charge higher interest that’s why construction loan rates tend to exceed traditional mortgage rates.

How are the rates determined?

Key drivers behind the rate you’ll be offered include:

- Borrower credit profile – credit score, debt-to-income ratio, liquidity.

- Project risk – builder experience, timeline, budget accuracy, location.

- Loan structure – term, fixed vs variable, draw schedule.

- Market conditions – broader interest rates, lender appetite, risk premiums.

What current rates look like

To give a ballpark: in 2025, construction loan APRs were reported between ~6.25% and 9.75% depending on many factors.

| Scenario | Approximate Rate | Notes |

| High-credit borrower, simple build | ~6%–7% | Lower risk, strong terms |

| Moderate risk or local market | ~8% | More buffer for lender |

| Higher risk, long term or speculative build | ~9%+ | Lenders demand premium |

Types of Construction Loans & Their Rate Implications

Construction-to-Permanent Loan

This loan starts as a construction loan then rolls into a long-term mortgage. The benefit: fewer closings, possibly locking in a rate early.

It may allow you to secure better construction loan rates if the permanent mortgage rate is good and you lock early.

Stand-Alone Construction Loan

You finance the build, pay it off or convert later. More risk: two closings, uncertain permanent financing. This risk often means higher rates.

Owner-Builder Construction Loans

When you act as your own contractor the lender sees higher risk due to builder capacity. Rate premiums apply. See the section on owner builder construction loans further below.

Business or Commercial Construction Loans

For non-residential builds (office, retail, industrial) the risk profile is higher, required equity may be larger, and thus rates for a commercial construction loan may be higher.

How to Get the Best Construction Loan Rates

Improve your financial position

- Boost your credit score and reduce debt.

- Have a detailed, realistic budget and timeline with contingency.

- Choose an experienced builder, submit full plans and specs.

- If you already own land, put that equity-in to reduce loan risk.

Shop around & negotiate

Don’t accept the first quote. Compare multiple lenders, ask about:

- Fixed vs adjustable rate options.

- Draw schedule and how interest accrues.

- Rate locks or conversion terms (especially for construction-to-permanent).

- Fees, closing costs, and points (which affect effective rate).

Understand rate structure and term

Because construction loans are short term, often interest-only, it’s vital to:

- Start with a realistic timeline to avoid extensions (which raise cost).

- Consider whether you lock in permanent rate early.

- Calculate total cost including interest only phase and subsequent mortgage.

Use the right calculator

Use a home construction loan calculator to model scenarios: interest-only phase, then conversion to mortgage helps compare loans and visualize the impact of rate differences.

Key Metrics & How They Affect Rates

Loan-to-Cost (LTC) & Loan-to-Value (LTV)

Lenders assess how much money they are putting relative to project cost (LTC) or end value (LTV). Higher ratios = more risk = higher rates

Duration and risk of timeline

Longer build periods increase risk of cost escalations or market shifts expect higher rates. A quick, standard project is viewed more favourably.

Type of collateral & exit strategy

If the project has pre-leased space or a guaranteed buyer, lenders feel safer and rates may be lower. Pure speculative builds attract risk premiums.

Market interest rate trends

Look at current baseline & risk premium. For example:

In Q1 2023 rates on A-D & C loans climbed to ~11% for speculative single-family construction. Knowing market benchmarks helps you assess if your quoted rate is fair.

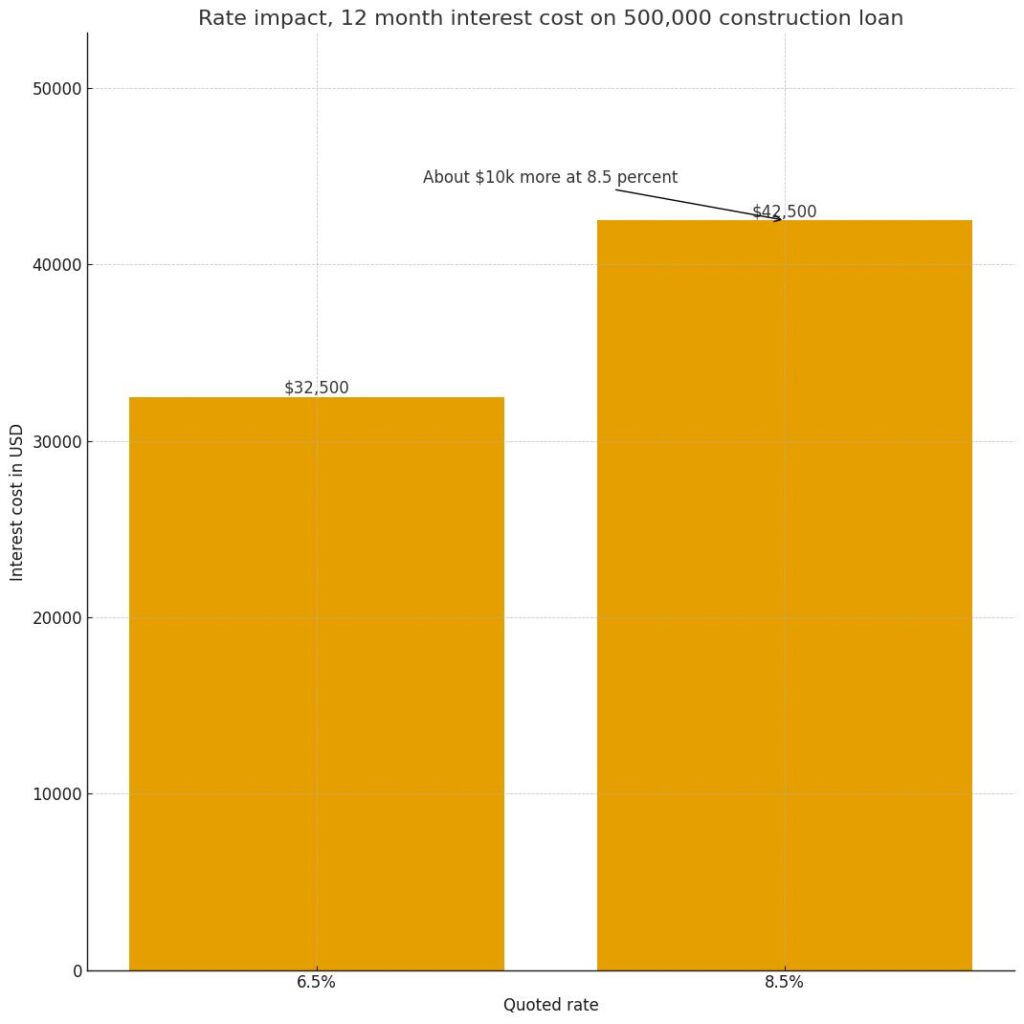

Rate Impact: Real-World Scenario & Cost Comparison

Example cost comparison

Assume you borrow $500,000 for 12-months construction phase with interest only, then convert to 30-yr mortgage.

| Rate | Interest cost during construction phase (12 mos) | Effect on monthly payment after conversion* |

| 6.5% | $500K × 6.5% ≈ $32,500 | Lower than higher rate scenario |

| 8.5% | $500K × 8.5% ≈ $42,500 | $10k higher cost just in year one |

Assumes similar conversion rate; higher initial cost reduces your fund for other project needs or contingency.

Specialized Use-Cases

If you need a commercial construction loan for a non-residential project, expect added factors: zoning, market lease rates, tenant risk, larger draws. Rates often trend higher than residential builds.

Owner Builder Construction Loans

When you act as builder, lenders add risk margin. A dedicated section on owner builder construction loans shows what you must prepare: builder credentials, contingency plan, more detailed budget.

Business Construction Loan

For businesses expanding facilities or building a new outlet a business construction loan may apply. Rates depend on business credit, cash-flow, collateral, and project viability.

Home Construction Loan Calculator & Modelling

Using a calculator

A home construction loan calculator helps model:

- Interest only phase cost

- Conversion to mortgage payments

- Impact of rate changes

Input key variables: loan amount, interest rate, draw schedule, term length.

Example: scenario modelling

- Loan amount: $400,000

- Phase one (12 mos) interest-only at 7.5% → $30,000 interest.

- Then convert to 30-yr at 5.5% → monthly payment ~$2,270.

Compare against 8.5% interest phase and 6.0% conversion rate to see effect of rate variances.

FAQs

Q: Can I lock in a rate for the construction phase?

Yes, many lenders offer a rate lock for fixed construction loans, giving protection against rate spikes.

Q: Why are construction loan rates higher than standard mortgage rates?

Because construction is riskier: incomplete collateral, potential delays or cost overruns, uncertain final valuation.

Q: Does better builder experience help lower rates?

Absolutely. A lender’s risk assessment includes builder track-record, budget realism, and timeline credibility.

Q: How small a margin can affect total cost?

Even a 1 % higher rate on a $500k loan over 12 months adds $5,000 more interest than a 1 % lower rate scenario. Cumulatively this affects margins, contingencies and profitability.

Summary & Next steps

Securing the best construction loan rates involves preparation, smart modelling and negotiation. Focus on presenting a strong borrower profile, a realistic and well-documented project plan, and compare lenders aggressively. Whether you go for a standard residential build or a larger scale business- or commercial-oriented project (such as a commercial construction loan or business construction loan), the same principles apply. Use a home construction loan calculator to model variables. If you’re acting as your own builder explore owner-builder construction loans carefully.

By emphasising clarity, structuring your loan correctly, and securing competitive terms you give your project the financial foundation it needs to succeed.